|

|

|

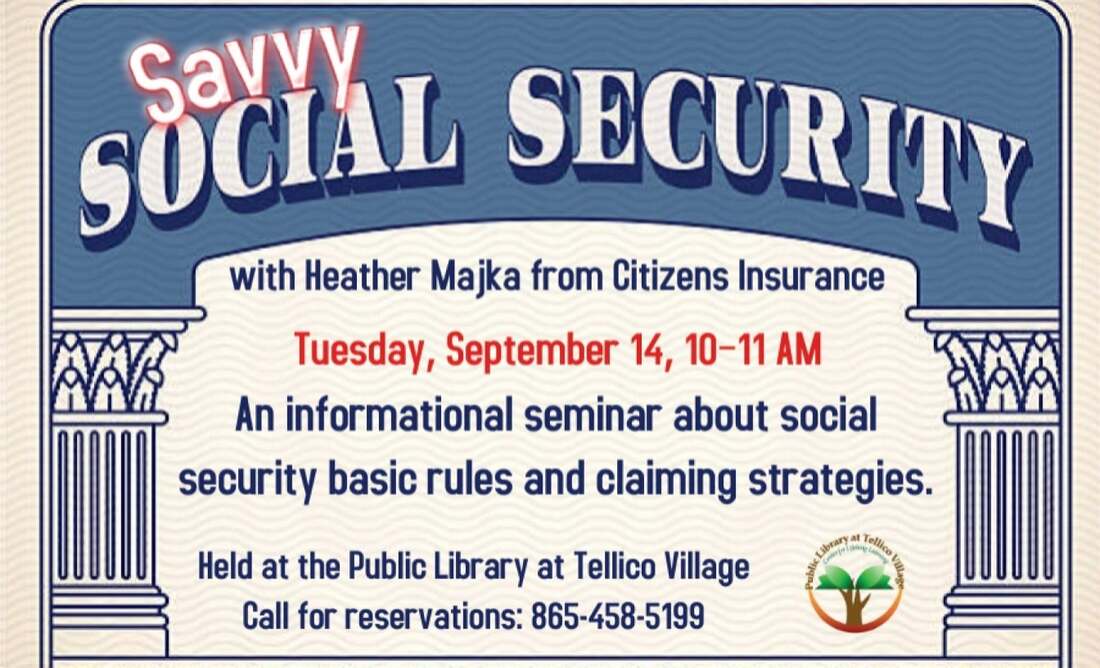

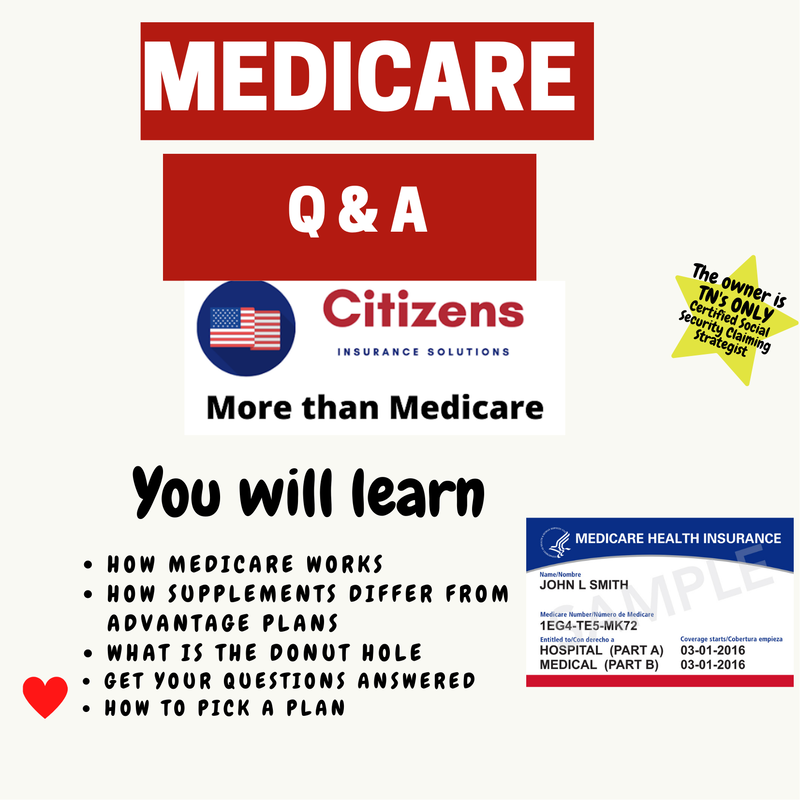

Join Heather Majka, Tennessee's only Social Security Claiming strategist for basic rules and filing strategies when filing for Social Security retirement. In just 30 minutes learn:- How to decide when to collect your benefits. - How to coordinate benefits with your spouse. - The Social Security options available to divorcees. - How the death of a spouse affects your Social Security benefits. - How work affects your benefits. - How your benefits are taxed and what you can do about it.  Medicare Q&A at the Public Library in Tellico VillageJoin our experts for this free public event but SPACE is LIMITED. You must call the library to RSVP as space is limited. 865-458-5199  Medicare and Cobra Cobra is temporary insurance that allows people to remain on their group health plan after leaving employment for up to 18 months. It is the same health insurance as before except you pay 102% of the premium (including what the employer was contributing). This can be the best option coverage-wise and even pricewise for some if under 65. If you are 65 or older and you or your spouse is offered COBRA, YOU MUST GET Medicare to avoid any penalties. Medicare DOES NOT consider COBRA coverage as good or better than Medicare (“not creditable”). What’s worse if you do NOT enroll in Medicare not only will you be penalized but COBRA will not pay your bills because they are secondary. When an insurance company is secondary that means that their contract and applicable laws dictate that they reduce their payment by the amount the first (primary) company would pay their share and that the second company pays only AFTER the first company. The Medicare Secondary Payer rules are complex. Much of the bill-shuffling takes place behind the scenes. If you are 65 and over, you can apply for Medicare at ANY time (while covered by employer health insurance/group health insurance). You also have up to 8 months to sign up for Medicare when your group coverage ends. The problem with signing up after coverage ends is that YOU WILL have a lapse in health insurance UNLESS you take Cobra. Most HR personnel and the average person do not realize that COBRA is not as good as Medicare and that YOU should sign up for Medicare before you (or your spouse) leave your employer. Here is the bottom line: RETIREMENT AFTER 65 = SIGN UP for Medicare (whether you are taking COBRA, Medicare Supplement, Medicare Advantage, Tricare, VA, or your employer’s retirement plan). Heather Majka, CPCU, CSSCS Doctors & Medicare The biggest concern most people have when switching to Medicare is how—and by whom—their health care services will be delivered. Will you still be able to see the same doctor? If you don’t currently have a primary care doctor, will you be able to get one under Medicare? What if you need a specialist? Will you have any say in choosing that specialist, and will the bills be covered under Medicare? When you keep original Medicare as your primary insurance (and you may or may not choose to buy a Medicare supplement also known as a Medigap plan) - the federal government pays your doctors (they hire a contractor to do it on their behalf). A recent survey from KFF (Kaiser Family Foundation) showed that only 1% of providers nationwide do NOT accept Medicare patients. That does not include providers that accept Medicare but do not accept new patients with Medicare. Every three months Medicare sends out a summary notice to show you all claims presented and paid. Learn more here. When you choose a Medicare Advantage plan, the private insurance companies pay your doctors, hospitals, etc. Providers have to be in the plan network and rules must be followed for your care to pay for. Nationwide 46% of providers participate in a Medicare Advantage network. Important questions to ask before selecting a Medicare Advantage plan are:

Learn more about Medicare Supplement plans here, and learn more about Medicare Advantage plans here. No matter which way you receive your Medicare benefits (even if you have retirement health insurance, Federal Insurance, Tricare, VA, and more) we can help you and answer all of your Medicare questions. AuthorHeather Majka, Certified Social Security Claiming Strategist, CPCU Plan on spending $300,000 for healthcare in retirementThis year’s estimate marks a new milestone high, up 30% from 10 years ago when the amount was $230,000, but just 1.7% from 2020 ($295,000) as health care inflation has remained relatively flat over the last few years. Fidelity began measuring in 2002 to build greater awareness of estimated health care costs and the importance of starting to plan and save early to meet those anticipated expenses. Since then, the estimate has risen a total of 88% (from $160,000). Fidelity’s estimate assumes both members of the couple are enrolled in traditional Medicare Parts A and B, along with a Part D drug plan.

According to Fidelity, a 65-year-old, opposite-gender couple retiring this year can expect to spend $300,000 in health care and medical expenses throughout retirement. For single retirees, the 2021 estimate is $157,000 for women and $143,000 for men. Fidelity’s annual release of health care costs in retirement provides an opportunity to remind clients that:

A message from Andrew Saul, Commissioner of Social Security:

About a year ago, I took the unprecedented step closer to our offices to the public. I did this to keep our employees and you—the public we serve—safe. As we enter year two of the COVID-19 pandemic, vaccines and other precautionary measures give us cause for hope. For now, we will continue our current safety measures as described in our COVID-19 Workplace Safety Plan. This plan is iterative, and we will update it as we receive additional government-wide guidance and information from public health experts in the Centers for Disease Control and Prevention. We understand that the public wants to engage with us on some matters in person, and our local offices are integral to our communities. We also know that not everyone can conveniently come to us in person and that when you do visit, you want the process to be efficient. For example, we may need evidence from you, but we do not need to interview you in person. We are currently testing drop box and express appointment options for the public to bring in the documentation. Often, you only need to know your Social Security number and do not need a physical Social Security card. However, if you do need to replace your card, we are testing video appointments if you need a new Social Security card but do not need to change any of the information in our records. Although ideas like these began as solutions during COVID-19, we are considering how they could improve service in the future. Some of these concepts also allow us to consider how we might continue to use telework, something that most organizations and companies have depended on during the COVID-19 pandemic, to drive longer-term operational efficiencies like reducing space. We could use those savings to provide you more online service options and hire more people to serve you more quickly as well as retain outstanding employees. We will continue to engage our managers, employees, and unions on ways we could use telework to improve customer service and other issues. You can find the full statement, and links to helpful resources, here.  Status of the Medicare Trust Fund There has been a certain amount of educated speculation about the effect of COVID-19 on the Social Security and Medicare systems. The 2020 OASDI Trustees Report, which was prepared before the pandemic gained a foothold and showed financial results through 2019, projected an exhaust date of 2035 for the combined OAS and DI funds. In April, Alicia Munnell of the Center for Retirement Research at Boston College issued a brief saying that if the COVID-19 economic collapse causes payroll taxes to drop by, say, 20% for two years, the depletion date would move up by about two years, to 2033.The latest weigh-in has come from the Congressional Budget Office (CBO). Its September 2020 report, CBO Outlook for Major Federal Trust Funds 2020 to 2030, projects the following exhaust dates:

It should be noted that when Congress and the president are planning their spending, they use the unified budget perspective. Rather than attaching an expenditure to the earmarked receipts (e.g., payroll taxes), the expenditures are based on the underlying authorizing laws. Both Social Security and Medicare are mandatory expenditures, making up about 60% of the total federal budget. This means they are protected from the appropriations process. The only way these expenditures can be reduced is to change the authorizing laws, which requires a 60-vote majority in the Senate. If the trust funds were to run dry, the United States would still be obligated to pay Social Security and Medicare benefits. The trustees, in their annual reports, generally say that when the trust funds run out, payroll taxes will be sufficient to pay X% of benefits (depending on which trust fund they are talking about). But the Social Security Act of 1935, as amended, requires benefits to be paid. There would be a conflict between two federal laws. Since we’ve never been in this situation, it’s impossible to know how it would be resolved.  On March 11, 2021 Biden passed the American relief act at a price tag of $1.9 trillion. This act will: The highlights:

Author: Heather Majka, owner of Citizens Insurance Solutions Tennessee’s only Social Security Claiming Strategist.

Can Congress cut the budget for Social Security?

No. Medicare and Social Security are MANDATORY expenses! Mandatory spending pays for U.S. federal programs that have already been established by Congress under so-called authorization laws. These laws both establish the federal programs and mandate that Congress must appropriate whatever funds are needed to keep the programs running. In other words, Congress cannot reduce the funding for these programs without changing the authorization law itself. Social Security and Medicare are the major mandatory spending categories. Clients who are worried that Congress can just decide to cut Social Security or Medicare benefits as part of the budget process – the way they play with defense spending and food stamps – need not worry. Because these programs involve mandatory spending, they cannot be cut without changing the authorization laws underlying them. This would take a 60-vote majority in the Senate. We’ve been saying for years that Social Security benefits for baby boomers are not jeopardy. Social Security is completely self-financed. Payroll taxes are deposited into a dedicated trust fund, along with income taxes on benefits and interest on the securities in the trust fund. The trust fund currently holds about $2.8 trillion in excess cash (currently invested in special-issue Treasury securities), an amount that will gradually be drawn down as baby boomers retire. By 2034 assets will be depleted and income will be sufficient to pay about 79% of promised benefits, under the trustees’ intermediate-cost projections. Social Security does need to be reformed in some way. The trustees have been telling us this for years. If it’s not, the trust fund will be exhausted in 2034 and payroll taxes will cover only about 77% of promised benefits. No one wants an across-the-board benefit cut in 2034. There are great reform measures proposed (and will likely be voted on closer to 2034) view them here. View Social Security’s current solvency here. Medicare is the largest government health program and the federal government is the largest payor of health services. Can Congress cut the budget for Social Security?

No. Medicare and Social Security are MANDATORY expenses! Mandatory spending pays for U.S. federal programs that have already been established by Congress under so-called authorization laws. These laws both establish the federal programs and mandate that Congress must appropriate whatever funds are needed to keep the programs running. In other words, Congress cannot reduce the funding for these programs without changing the authorization law itself. Social Security and Medicare are the major mandatory spending categories. Clients who are worried that Congress can just decide to cut Social Security or Medicare benefits as part of the budget process – the way they play with defense spending and food stamps – need not worry. Because these programs involve mandatory spending, they cannot be cut without changing the authorization laws underlying them. This would take a 60-vote majority in the Senate. We’ve been saying for years that Social Security benefits for baby boomers are not jeopardy. Social Security is completely self-financed. Payroll taxes are deposited into a dedicated trust fund, along with income taxes on benefits and interest on the securities in the trust fund. The trust fund currently holds about $2.8 trillion in excess cash (currently invested in special-issue Treasury securities), an amount that will gradually be drawn down as baby boomers retire. By 2034 assets will be depleted and income will be sufficient to pay about 79% of promised benefits, under the trustees’ intermediate-cost projections. Social Security does need to be reformed in some way. The trustees have been telling us this for years. If it’s not, the trust fund will be exhausted in 2034 and payroll taxes will cover only about 77% of promised benefits. No one wants an across-the-board benefit cut in 2034. There are great reform measures proposed (and will likely be voted on closer to 2034) view them here. View Social Security’s current solvency here. |